As Tilray Expands Its Medical Cannabis Business, Should You Buy, Sell, or Hold TLRY Stock?

Tilray’s (TLRY) aggressive expansion into Germany’s medical cannabis scene signals a drive to claim more of the global spotlight. The company posted fiscal 2025 highlights that include $821 million in net revenue, up 4%, and a jump in cannabis segment gross margin from 33% to 40%. This financial delivery comes as Tilray strengthened its balance sheet, cutting debt by nearly $100 million and building a $256 million liquidity buffer.

All this is happening as the cannabis sector is gaining traction, as global market value could approach $444 billion by 2030. The recent surge in optimism, especially after high-profile endorsements and stronger legalization trends, has reignited momentum across medical cannabis players.

That’s why Tilray’s latest five-product rollout in Germany comes at such a pivotal moment. The question now is whether the launch makes TLRY worth a buy, a sell, or a hold. Let’s find out.

What TLRY’s Earnings Reveal

Tilray operates as a diversified cannabis and wellness company, focusing on medical cannabis, beverages, and other consumer products. The company currently does not pay a dividend. The stock price stands at $1.64, with a year-to-date (YTD) increase of 21.8%, though its 52-week performance shows a decline of 1.8%.

With a market capitalization of approximately $1.78 billion, Tilray is valued at a fraction of the sector median. Its price-to-sales (P/S) ratio is 2.17x compared to the sector median of 4.18x. The price-to-cash flow (P/CF) stands at 11.21x, below the sector median of 14.81x, while the price-to-book (P/B) ratio is 1.15x, significantly lower than the sector’s 2.78x median. These valuation metrics suggest Tilray trades at a discount relative to its cannabis peers.

Tilray’s fiscal year 2025 earnings, released on July 28, reflect steady progress despite strategic challenges. The company achieved net revenue of $821 million, increasing 4% from $789 million the prior year. That figure rises to $834 million when adjusted for constant currency. This revenue growth was partly tempered by a $35 million impact from international permit delays and strategic priorities in Canada, including a $15 million revenue hit from deemphasizing vape products. This helped Tilray preserve higher margins in more profitable segments.

While TLRY reported a net loss of $2.18 billion, this included a significant non-cash impairment of goodwill and intangible assets totaling $2.1 billion. Adjusted net income rose 45% to $9 million, with adjusted earnings per share stable at $0.01. Adjusted EBITDA came in at $55 million, slightly below the prior year.

The company holds a strong liquidity position, with $256 million in cash and marketable securities. It reduced bank indebtedness by $10.9 million and cut net long-term debt substantially, repaying nearly $100 million in convertible debt year-to-date. Tilray’s financial discipline and strategic recalibration position it well for further growth.

What’s Driving Tilray’s Momentum

The sector’s spotlight is locked on Tilray after an apparent endorsement of medical cannabis by President Donald Trump. The president shared a video on Truth Social promoting cannabidiol’s potential to “revolutionize senior healthcare,” estimating a possible $64 billion in annual medical cost savings. This, combined with previous public comments on reclassification, has lit up investor optimism. It’s fueling expectations for broad adoption of CBD products and triggering hope for friendlier regulatory changes, especially moves that could see marijuana reclassified and make more room for companies like Tilray to grow.

It’s no surprise the timing favors Tilray. The company just expanded its premium craft cannabis portfolio in Germany with five new locally produced cannabis flower products. These are crafted at the EU-GMP-certified facility in Neumünster and launched as part of the BfArM in-country cultivation program. The new entries include a wide range of THC potencies: THC30 TRM (Triangle Mints), THC28 TRM (Triangle Mints), THC28 PPV (Platinum Pave 34), THC25 PPV (Platinum Pave 34), and THC22 SNS (Sunset Sherbet).

Each product aims for precision and quality, bringing uniform dosing and reliability to German pharmacies. Tilray’s production meets strict EU-GMP standards, ensuring patients get consistency and safety with every prescription. This expansion is about Tilray deepening its roots in Europe’s biggest and most important medical cannabis market.

What Analysts and Estimates Imply

Tilray’s upcoming earnings release, scheduled for Oct. 9, holds considerable significance. Analysts estimate the adjusted earnings per share for the current quarter to be -$0.03, matching the estimate for the next quarter in November. For the full fiscal year ending May 31, 2026, the average earnings estimate dips to -$0.11 per share, reflecting some caution for future profitability.

Despite this, management’s guidance points to optimism. Irwin D. Simon, Chairman and Chief Executive Officer (CEO), underscored the company’s potential in cannabis, beverage, and wellness product lines as key growth drivers for fiscal 2026.

Tilray expects its adjusted EBITDA for the fiscal year 2026 to range between $62 million and $72 million. This represents a growth of 13% to 31% compared to fiscal 2025, signaling that operational improvements could start translating into stronger financial performance.

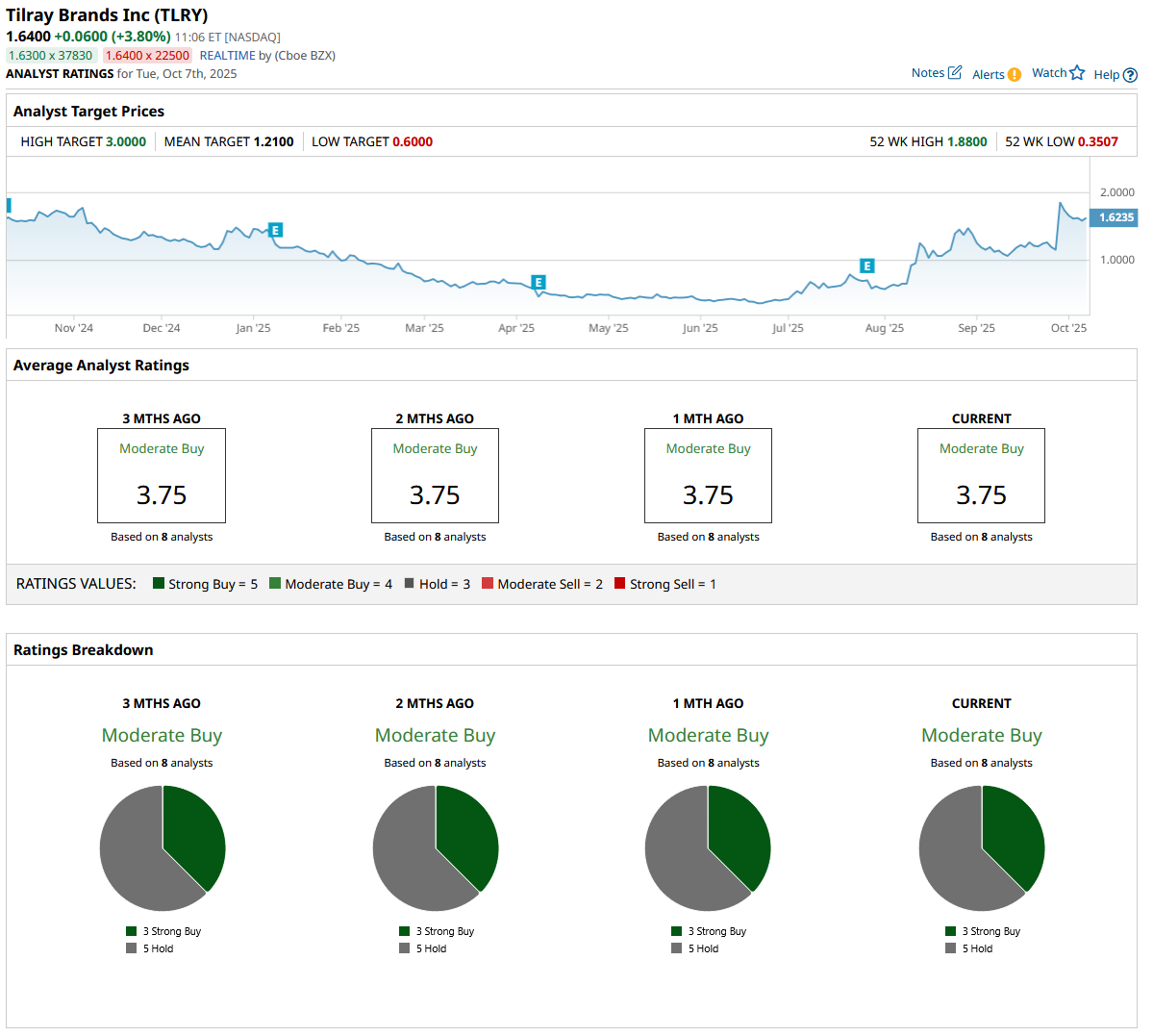

The consensus among analysts, based on eight surveyed experts, skews moderately bullish with an overall “Moderate Buy” rating. They assign an average price target of $1.21 to TLRY stock, implying a downside potential of approximately 26%.

Conclusion

Tilray has made some bold moves and generated a real buzz with its German expansion and renewed sector optimism. But even with impressive product launches and a more confident balance sheet, analysts see the near-term upside as limited, with a target below today’s price. Shares could hold steady or drift slightly lower as the company works through its new business strategy and proves consistent earnings. For now, TLRY looks best as a hold for patient investors waiting on clear profits and regulatory wins, but if momentum builds, this stock could surprise to the upside.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.