Supermicro Stock Is Gaining Steam. Can the Rally Continue?

/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

Supermicro (SMCI) stock has gained steam, surging over 35% over the past month as the company’s growth rate is expected to accelerate. The rebound comes after a post-earnings slump, when slowing sales momentum and lower-than-expected outlook briefly cooled enthusiasm for one of the market’s favorite AI hardware plays.

SMCI Stock: From Post-Earnings Slump to Renewed Optimism

Notably, Supermicro has seen its sales and earnings skyrocket thanks to artificial intelligence (AI)-driven demand. Its high-performance servers and storage systems are engineered to power demanding AI workloads and applications, and have witnessed solid demand.

Fiscal 2024 was a blockbuster year for the company, with revenue expanding at an exceptional pace. However, growth moderated sequentially in fiscal 2025. In the fourth quarter of fiscal 2025, Supermicro reported revenue of $5.8 billion, up just 7.4% year over year, a sharp slowdown compared to earlier quarters, when growth regularly topped double or even triple digits. Margins also came under pressure, as tariffs and manufacturing costs weighed on profitability.

Adding to the challenges, temporary headwinds, such as capital constraints, had impacted production capacity. At the same time, evolving design requirements from large AI customers delayed some shipments. Rapid innovation cycles in AI hardware have also lengthened purchasing decisions, as companies wait for the latest, most efficient systems before committing to major orders.

Despite these short-term challenges, Supermicro’s growth is likely to accelerate in the coming quarters. The company stated that it has resolved earlier funding issues and expects previously delayed customer orders to be fulfilled in the upcoming quarters. Its large and enterprise customer base is expanding rapidly as well, reflecting that the demand for its systems remains solid.

Supermicro Targets High-Margin Areas

Looking ahead, Supermicro is broadening its reach beyond hyperscale AI into higher-margin areas such as enterprise, Internet of Things (IoT), and telecommunications. The company has been investing heavily to tailor its next-generation servers and storage systems for hybrid cloud, edge computing, and enterprise-level AI applications. Its recently launched enterprise service program, offering 24/7 global support for advanced data center deployments, further supports this strategic shift.

In IoT, Supermicro’s embedded and edge systems are gaining traction in industries ranging from manufacturing and healthcare to smart cities and telecom. New partnerships in AI at the edge and telecom innovation are expected to accelerate this diversification, helping the company build a more resilient, profit-driven business model.

Further, Supermicro’s global manufacturing network provides a competitive advantage. With major facilities across the U.S., Malaysia, Taiwan, and the Netherlands, the company can deliver complete rack-scale systems and data center solutions efficiently while reducing exposure to trade-related risks. This international footprint enhances its supply chain flexibility and allows it to adapt quickly to regional demand shifts.

Super Micro Strengthening Technology Leadership

Technologically, Supermicro continues to lead the AI infrastructure market with platforms optimized for the latest Nvidia (NVDA) and Advanced Micro Devices (AMD) GPU architectures. Its flagship X14 and H14 GPU systems deliver top-tier performance and energy efficiency, addressing both massive AI training clusters and enterprise workloads.

The company’s Datacenter Building Block Solutions (DCBBS), its modular, energy-efficient infrastructure solutions, are now shipping in large volumes to meet rising demand. These innovations are expected to play a key role in driving the next leg of revenue growth.

The Road Ahead: Can the Rally in SMCI Stock Continue?

Supermicro’s management expects at least $33 billion in total revenue in fiscal 2026, up about 50% year-over-year. This outlook reflects a sequential acceleration in growth rate, supported by its expanding customer base, product innovations, and scaling of new product lines such as DCBBS total solutions.

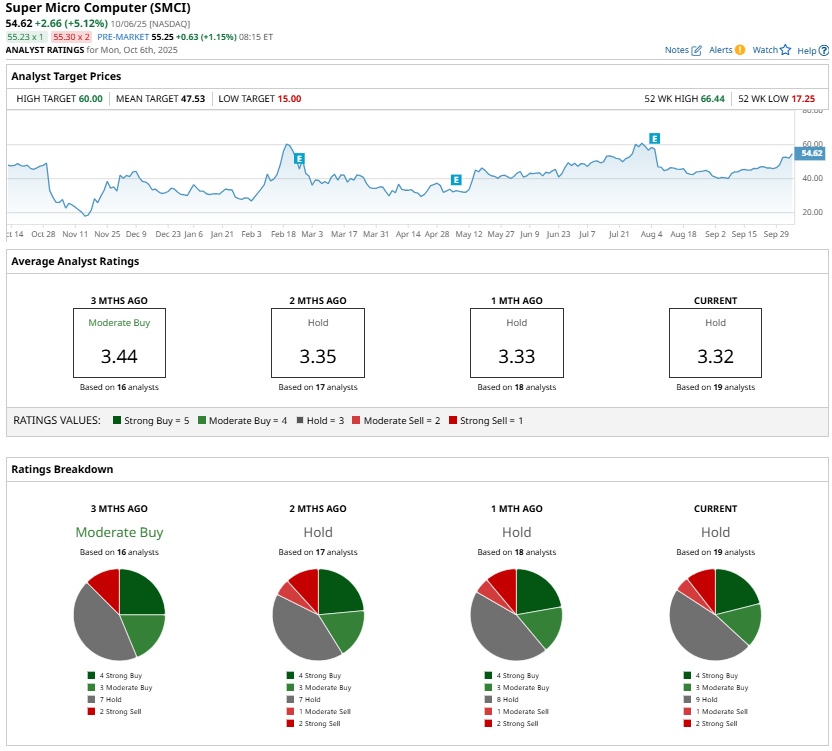

While analysts maintain a cautious “Hold” consensus rating on SMCI stock, the company’s ability to rebound from a post-earnings slump reflects strong underlying demand for its AI-driven server and data center solutions. With production constraints easing, customer orders returning, and its focus on diversifying into higher-margin markets such as enterprise, IoT, and telecommunications, Supermicro is poised to deliver solid growth, which could support its share price.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.